When War Becomes a "Black Swan" for the Supply Chain

In March 2026, the conflict between Israel and Iran escalated abruptly, resulting in the effective closure of the Strait of Hormuz—the "throat of the world" through which approximately 20% of global oil shipments pass. For the High-Density Polyethylene (HDPE) pipe industry, this geopolitical storm was not merely distant international news, but a tangible crisis directly impacting cost structures, supply chain security, and pricing mechanisms.

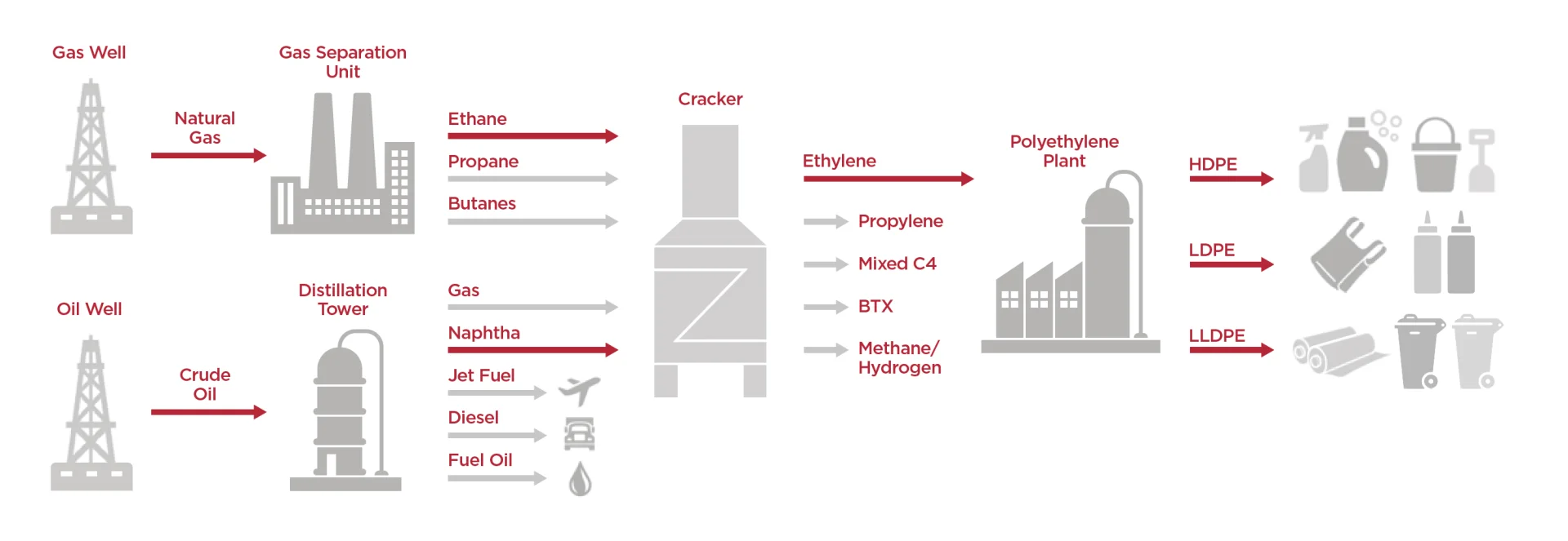

The primary raw material for HDPE pipes is ethylene, the production of which relies heavily on naphtha—a key byproduct of petroleum refining. As shipping traffic through the Strait of Hormuz plummeted from a daily average of 130 vessels to a mere 6—a staggering decline of 95%—the very foundations of the entire petrochemical supply chain began to crumble.

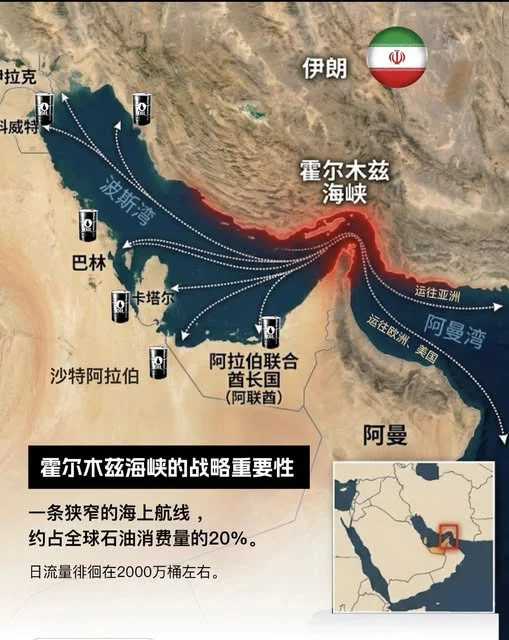

Geographical Features of the Strait of Hormuz

The Strait of Hormuz is aptly described as the "World's Oil Jugular Vein," for the following reasons:

Uniqueness: It serves as the sole maritime conduit for the export of oil from the Persian Gulf, with no alternative shipping routes available.

Narrowness: At its narrowest point, the strait is merely 21 miles wide, necessitating that large oil tankers pass through in single file.

Topographical Enclosure: It is flanked to the north by the Iranian coastline (characterized by mountainous and steep terrain) and to the south by Oman's Musandam Peninsula.

Navigational Channel Characteristics

Main Channel: The actual navigable width available for large oil tankers is limited to approximately 2 miles (3.2 kilometers).

Two-Way Traffic: Tankers are required to navigate within designated lanes, effectively creating a "one-way street" effect at sea.

Shallow-Water Restrictions: In certain areas, water depths are insufficient; consequently, Very Large Crude Carriers (VLCCs) must either reduce their cargo loads or take a detour.

Geographical Vulnerability to Blockade

The geographical characteristics of the Strait of Hormuz render it highly susceptible to military blockade:

Extreme Narrowness: At a width of just 21 kilometers, the entire strait falls well within the coverage range of shore-based firepower, given modern military technology.

Terrain Advantage for Defense: The Iranian coastline is characterized by rugged mountainous terrain, which facilitates the strategic deployment of anti-ship missiles and radar systems.

Fixed Shipping Lanes: Oil tankers have no alternative routes and are therefore inevitably exposed to both surveillance and potential strikes.

Quantification of Strategic Value

Share of Global Oil Transport: Approximately 20% of global oil consumption passes through this strait.

Liquefied Natural Gas (LNG): Qatar is the world's largest LNG exporter, and nearly 100% of its exports rely on this strait.

Average Daily Vessel Traffic: Under normal conditions, approximately 130 vessels of various types pass through daily.

During the 2026 Crisis: Traffic plummeted to a mere 6 vessels—a decline of 95%.

How War Breaches the Cost Defenses of HDPE Pipelines

1. The "Three-Tiered Leap" in Raw Material Price Transmission

Following the closure of the Strait of Hormuz, prices for energy and chemical raw materials have exhibited a classic "supply chain transmission" effect:

Tier 1: The Violent Surge in Crude Oil Prices

Brent crude oil prices skyrocketed from $72 per barrel prior to the conflict to over $110. Should the Strait remain blockaded, market forecasts suggest prices could breach the $150 mark—or even touch $200. Morgan Stanley notes that this supply disruption impacts approximately 20% of the global oil supply, a severity level twice that of the 1956 Suez Canal Crisis.

Tier 2: A Structural Shortage in Naphtha Supply

In the Asian market, 76% of the crude oil flowing through the Strait of Hormuz is destined for nations such as China, Japan, South Korea, and India—precisely the core hubs of the global petrochemical industry. As the primary feedstock for ethylene production, naphtha has seen its price increases outpace even those of crude oil. Prime Polymer Co., Ltd.—a subsidiary of Japan's Mitsui Chemicals—has announced that, effective April, it will raise the prices of polyethylene and polypropylene by over 90 yen per kilogram. This represents an overall price hike of approximately 30%, exceeding the increases observed during the Russia-Ukraine conflict in 2022.

Tier 3: A Comprehensive Surge Across the Polyethylene Market

Within just one week of the conflict's outbreak, the domestic polyethylene market witnessed a broad-based rally across all segments. The benchmark plastics futures contract on the Dalian Commodity Exchange climbed from 7,020 yuan/ton to 7,405 yuan/ton, marking a cumulative increase of 5.48%. In the spot market, High-Pressure Low-Density Polyethylene (LDPE) saw a weekly gain of 6.2%, while Linear Low-Density Polyethylene (LLDPE) rose by 5.9%. As a vital member of the polyethylene family, HDPE prices have likewise surged significantly in tandem.

2. The "Supply Gap" Crisis in the Supply Chain

The Middle East serves not only as a major hub for oil exports but also as a critical nexus for the global trade of chemical products. By 2025, the Middle East's share of the global trade volume for key chemical commodities—such as methanol and ethylene glycol—is projected to range between 25% and 50%, with the vast majority of these exports flowing into Asian markets. Currently, several manufacturers in the Middle East have announced that they are unable to fulfill product deliveries due to *force majeure* events.

For HDPE pipe manufacturers, this entails the following consequences:

**Surging Raw Material Procurement Costs:** Ethylene prices have risen sharply—driven by a shortage of naphtha—directly driving up the cost of HDPE resin.

**Disrupted Supply Flows:** South Korea has already experienced shortages of plastic products—such as garbage bags—stemming from interruptions in ethylene feedstock supplies; HDPE pipe production faces a similar risk of raw material shortages.

**Inventory Management Dilemmas:** Extreme price volatility makes it difficult for companies to determine appropriate inventory levels; maintaining excessive stock exposes them to the risk of price depreciation, while insufficient stock runs the risk of halting production.

Multidimensional Impacts on the HDPE Pipe Industry

1. The Cost Front: From "Calculable Risk" to the "Disappearance of Certainty"

Serbian President Vučić has warned that the essence of the current shock is not merely a rise in prices, but rather the "disappearance of certainty." Over the past few weeks, prices—spanning everything from crude oil to naphtha and polyethylene—have surged almost in unison; yet, following a temporary ceasefire agreement between the U.S. and Iran, crude oil prices plummeted just as rapidly. Such violent fluctuations render it impossible for enterprises to forecast their costs, supply levels, and order volumes even three months in advance.

For the HDPE pipe industry, this uncertainty manifests in the following ways:

Invalidated Quotations: Pipe engineering projects typically require price quotes to be submitted months in advance; however, the drastic volatility in raw material prices has rendered these quotation strategies ineffective.

Contractual Risks: Signed fixed-price contracts now face the risk of massive financial losses, making the trade-off between the costs of breaching a contract and the losses incurred by fulfilling it a difficult dilemma to resolve.

Cash Flow Strain: The procurement of raw materials often requires upfront payments or immediate cash settlement, while the payment collection cycle from downstream clients has lengthened, placing significant pressure on the cash flow of small and medium-sized enterprises (SMEs).

2. The Demand Front: The "Extreme Contrasts" of Infrastructure Investment

HDPE pipes are primarily utilized in sectors such as municipal water supply and drainage, gas transmission, agricultural irrigation, and mining. The economic shocks triggered by geopolitical conflicts are currently reshaping these downstream demand patterns:

Short-Term Stimulus Factors:

Energy security strategies are prompting nations to accelerate investment in energy infrastructure, which may drive increased demand for certain types of piping.

Amidst the trend toward supply chain regionalization, the demand for localized production is on the rise.

Medium- to Long-Term Inhibiting Factors:

Global GDP growth forecasts for 2025 have been downgraded from 2.9% to 2.6%, leading to anticipated cuts in infrastructure investment budgets.

Driven by inflationary pressures, central banks worldwide are maintaining high interest rates; the resulting rise in financing costs is dampening the commencement of new engineering projects.

The risk of disruptions within the chemical industry supply chain is causing delays or cancellations for a number of engineering projects.

3. The Competitive Landscape: The "Redistribution" of Supply Chain Profits

Kelly Chen, President of BASF Asia Pacific, has noted that the crisis in the Gulf region is sending shockwaves through the entire chain—from energy sources to raw materials and ultimately to chemical products—and that profits within this supply chain are expected to undergo a "redistribution." Upstream sectors—specifically oil and gas extraction, coal-based chemical production, and cracking enterprises utilizing ethane and butane feedstocks—are poised to benefit, while downstream terminal manufacturing operations and cracking enterprises reliant on naphtha feedstocks face mounting pressure. For the HDPE pipeline industry:

Enterprises possessing upstream resources—such as those strategically positioned in coal-to-ethylene production (leveraging China's coal-based olefin capacity)—enjoy a distinct relative cost advantage.

Purely processing-oriented enterprises face a dual squeeze from soaring costs and contracting demand, resulting in a severe erosion of their profit margins.

Import-dependent enterprises—particularly those in Japan and South Korea relying on the Middle East naphtha route—are experiencing an exacerbation of their cost disadvantages.

HDPE Pipe Price Forecast and Scenario Analysis

Scenario 1: Short-term Reopening of the Strait (Within 1–2 Months)

Assumptions: U.S.-Iran negotiations make progress; the Strait of Hormuz reopens to navigation; and energy infrastructure sustains no severe damage.

Price Trends:

Short Term (1–3 months): HDPE prices remain high and volatile. Even if the Strait reopens, a massive "air pocket" has already formed within the supply chain; inventory gaps and logistical disruptions will keep petrochemical product prices elevated. HDPE resin prices are projected to rise by 20–30% compared to pre-conflict levels.

Medium Term (3–6 months): As supply chains gradually recover, prices will slowly retreat but remain above 2025 levels. Brent crude is expected to fall back into the $80–$90 per barrel range.

Finished HDPE Pipe Prices: Expected to rise by 15–25% compared to 2025 levels; the specific magnitude of the increase will depend on individual companies' bargaining power and the efficiency of cost pass-through.

Scenario 2: Medium-to-Long-term Closure of the Strait (3–6 Months)

Assumptions: The conflict persists; the Strait of Hormuz is effectively closed; and some energy infrastructure sustains damage.

Price Trends:

Crude Oil Market: Brent crude could surge past $150 per barrel; if the blockade persists for more than three quarters, the global economy will plunge into a severe recession.

Naphtha and Ethylene: The supply deficit for naphtha in Asia widens, and ethylene prices could double. The U.S. gains market share by leveraging its shale gas-based ethane cracking route.

HDPE Resin: Prices could rise by 40–60%, accompanied by tight supply.

Finished HDPE Pipes: Prices rise by 30–50%; however, the demand side may experience "demand destruction"—excessively high prices suppress actual demand, leading to project delays or a shift toward alternative materials (such as ductile iron pipes, PVC pipes, etc.).

Scenario 3: Extreme Case (Strait Closure Exceeds 6 Months)

Assumptions: The conflict escalates into a full-scale war; production capacity in major Middle Eastern oil-producing nations is severely damaged; and the global energy landscape undergoes a fundamental restructuring. Systemic Risks:

The global chemical industry supply chain faces its most severe supply disruptions since the oil crisis of the 1970s.

The HDPE pipe industry may face raw material rationing, leading to a drastic decline in capacity utilization rates.

Prices have lost their economic significance, and the market is shifting toward barter or long-term agreements to secure supply.

Finding Certainty Amidst Uncertainty

The crisis in the Strait of Hormuz serves as yet another reminder that in today’s deeply interconnected globalized world, geopolitical risks can instantly ripple through to the realm of even the most fundamental industrial materials. For the HDPE pipe industry, this crisis represents both a severe test and a catalyst for transformation and upgrading.

In the short term, price volatility and supply shortages will continue to plague the industry; in the medium term, the regional restructuring of supply chains will reshape the competitive landscape; and in the long term, the dual pressures of energy security and sustainable development will drive technological advancement within the sector.

As the UN Conference on Trade and Development (UNCTAD) has warned: "Disrupted energy flows, rising prices, slowing trade, and tightening financial conditions collectively exert broad pressure on the global economy." Amidst this storm, only those enterprises that build resilient supply chains, maintain financial stability, and pursue continuous technological innovation will be able to usher in a new cycle of growth once the crisis has passed.